By Richard Morey

March 2023

Something Smells: Shadow Banking

Something Smells: Shadow Banking

For some time, I have been stymied trying to find exactly where all the rotten corporate debt had gone. Year after year, I’ve scoured the corporate bond markets, but found only a fraction of the bad debt I knew was being created.

Beginning last year, a number of the best economists focused on debt started to release totals of what is called ‘shadow banking.’ Before examining the amount of total shadow banking debt and potentially misallocated capital, let’s first define the term. The official definition of shadow banking was recently formulated by the Financial Stability Board (FSB) as “the system of credit intermediation that involves entities and activities outside the regular banking system”.

The first exhaustive analysis of our shadow banking system came out late last year from the Bank of International Settlements (BIS), considered the “central bank of the central banks.” The numbers were astounding. The BIS said they had spotted more money lent through non-regulated, non-transparent markets, than through the entire US banking and regulated debt markets.

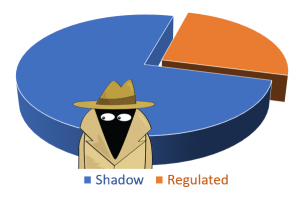

The main forms of shadow banking consists of hedge funds, private equity funds, various types of funds which create derivative packages of low-quality, non-traded corporate debt, and non-public, quantitative trading programs sponsored by brokerage firms and sold to large insurance companies and other institutional investors. Adding in non-transparent pension plan and insurance company loans and investments gives us a total of approximately $42 trillion in our shadow banking system. A debt liquidation which wipes out the debt that will never be repaid could easily lead to $15 trillion in losses.

In contrast, the entire regulated, traded corporate bond market is “only” $11 trillion – in quotes because that is by far the largest amount of corporate bond debt ever seen – yet of course it’s only one-quarter as large as the non-transparent, shadow banking lending channels.

traded corporate bond market is “only” $11 trillion – in quotes because that is by far the largest amount of corporate bond debt ever seen – yet of course it’s only one-quarter as large as the non-transparent, shadow banking lending channels.

Of that $11 trillion in regulated bonds, a minimum of $3 trillion has, in effect, already been lost. This is the amount of lower-quality bonds in which the money was loaned to companies who will never pay any of the principal back. Add in the $15 trillion in potential losses from the shadow banking side, and we get $18 trillion in losses, or roughly a startling 80% of one year’s entire GDP or economic output.

We could write a paper on the size of and risks inherent in each type of shadow banking. Instead, I’ll just discuss the one about which I know the most. These are large institutional trading programs They all have the same flaw – they tend to be “lemmings” who have predictable, industry-wide losses when markets become extreme. The trading programs are dangerously simplistic mathematical models used to invest many trillions of dollars today.

Look under the surface, and you find none of their models account for extreme market outcomes. Their programs tend to be very safe and consistent, with high risk-adjusted returns, during the good times. But much of their higher than normal returns in the build-up to a bubble are achieved by not insuring properly against a severe ‘black swan,’ in which one or more of the markets crumble. By design they never add this crucial protection – all the way to the bottom. Their algorithms end up being essentially identical, with none of them providing risk-control when most needed.

Because the institutional trading programs now move vast amounts of money – and they all have the same flaws – this sets the markets up for both severe losses and a time of high market volatility. In addition, when stress becomes large enough, nearly all the pension plans will also “break,” as they have now allocated large percentages into shadow bank financing.

Why do we expect large swaths of shadow banking to explode? Simple. Many have loaned massive amounts of money to companies likely to fail at any reasonable rate of interest. Inflation will therefore turn out to be the nail in the coffin of their trillions of dollars of misallocated capital. Their debt creations only work when the cost of money is so cheap every company with a pulse can get it.

While traditional bank assets have increased 35% to $148 trillion worldwide, nonbank financial companies have grown 61% to $185 trillion during the same period. By their name and nature, we have little to no idea where the blow-ups in shadow banking will occur. How could we, given that they are non-transparent? Nobody knows what they’re doing – including their investors in most cases.

It gives me great comfort to know that we have sensible hedging systems firmly in place. Managed futures trading programs are in stark contrast to the “lemming-like” quantitative trading programs used by huge institutional investors described above. The much smaller managed futures fund industry is carefully, mathematically designed to profit when major asset classes decline – the more markets that drop, the more the funds are designed to make. The historical record for managed futures shows they have performed as designed whenever risk hits – and especially when it then spreads.