By Richard Morey

June 2022

Exploring Managed Futures

Let’s start with a definition.

Let’s start with a definition.

MANAGED FUTURES are contracts to buy or sell, within four asset classes:

1. Equity

2. Fixed income

3. Commodities

4. Currencies

There are over 150 futures markets, including, for example, one for each major commodity, for each major currency, and for each major stock and bond market index. A managed futures fund may have 100 long positions which profit when the underlying price rises, and an equal amount of short positions which profit when it falls. The fund will typically also have most of its holdings (around 75%) in high-quality, short-term debt designed to add a stable percentage in annual return.

How do the funds decide which markets to own and which to sell? As you might expect, the answer differs for each fund, but all are highly complex trading programs based on massive amounts of market history, which often include behavioral psychology. They all employ mathematical algorithms based on recurring market patterns.

For example, if you look at the highest-returning managed futures mutual funds, you’ll find most are centered on the concept of reversion. The trading systems these funds employ are activated relatively early as a reversion begins:

The “trigger system” is based on rising or falling volatility. In terms of time, futures funds seek asset classes in the early stages of an extended (the longer the better) increase in volatility. A representative mutual fund in this category, called the Altegris Systemic Trend Fund, tells us they “…may experience the best conditions for profitable outcomes across multiple sectors and markets in multi-week and multi-month sustained trends.” Those trends can be traced by following the volatility measurements for each asset class. The systems then add in their historically based market filters to tell them when to enter and exit those markets as volatility rises and falls.

Translated into English, the above statement from Altegris means their managed futures fund is designed to make the most money when we have a crisis, with the largest profitable outcomes expected when the entire world economy and markets suffer most significantly.

You will note they don’t say they’ll have the best conditions for profit when the U.S. stock market goes down. To accurately do so would mean they had a correlation of a negative one with the stock market, and their value would rise every day stocks went down and fall every day they went up.

A simple, rigid formula like this would of course be a recipe for failure. Instead, managed future funds constantly monitor all 150+ futures markets (or a subset) for the best investment opportunities. They combine long and short positions in these asset classes to create a highly diversified portfolio designed to profit the most when markets enter large swings over periods of weeks or months (generally months).

Risk Control

If you Google “Managed Futures Funds,” you may end up with the impression they are all risky. However, the fund managers themselves would never use such a meaningless word as ‘risky,’ applied so broadly. Risk is involved in every investment. What matters is how careful and well-informed an investor is regarding risk. Is it being measured and monitored? Is the risk-management system robust enough to withstand rare events, the dreaded “black swans?” I believe the long track record of successful futures funds through past periods of instability and market turmoil should carry far more weight than superficial judgement or uninformed media bias.

First, keep in mind these funds have 75% of their holdings protected in short-term Treasuries and comparable securities. They combine their remaining long and short positions in dozens of markets, putting typically no more than 3-4% in any one asset class. They then calculate their risk level, setting their portfolio at the correct level of volatility over their preferred time periods.

First, keep in mind these funds have 75% of their holdings protected in short-term Treasuries and comparable securities. They combine their remaining long and short positions in dozens of markets, putting typically no more than 3-4% in any one asset class. They then calculate their risk level, setting their portfolio at the correct level of volatility over their preferred time periods.

Second, by not tying themselves to the stock market, or any other single market or preselected combination of markets, they are able to create funds with the best diversification features of any asset class. They only have a modest correlation to any other asset – in fact, nearly zero for both the U.S. stock and bond markets

To put this into simple numbers, the S&P 500 has volatility of 19.72 (Standard Deviation) over the last three years (through 5/23/22 – all data from Ycharts using 3-year standard deviation calculations), while the Vanguard Target Retirement 2025 Fund (targeting 60% in stock/40% in fixed income) comes in at 11.47.

In contrast, a managed futures portfolio consisting of an equal weighting of five of our favorite open-ended managed futures mutual funds has a score of 9.12. This means this portfolio would be assuming only 46% as much volatility as stocks and would have 20% less volatility than the Vanguard balanced fund designed for someone approaching retirement. (I will discuss potential problems with holding Vanguard’s retirement funds during periods of severe volatility below.)

How Much Can You Overweight the Best-Performing Managed Futures Funds?

In a crisis era the answer may be that you can’t overweight them. This is especially true when markets all around the world experience unusually high volatility over extended time periods.

From a pure risk-control standpoint, however, a standard deviation of even 9 may be too high for some conservative investors. I have argued for many years that Vanguard’s target funds are too aggressive when markets are stretched beyond their normal limits, and I believe this is especially true today.

Fortunately, it’s simple to reduce the risk level by capping managed futures at 65% of the portfolio. If the rest is split between a conservative long/short equity fund (HSGFX), a conservative short duration options trading fund (HRSAX), with a small 6% to gold and silver (CEF) and 6% to commodities (DCXIX), the volatility of the portfolio plunges down to 7.12.

We target a volatility “score” of only 7.12 today for one simple reason: We see the markets now undergoing a large transition which translates into increased risk. This is likely to lead to a sharp break in both the stock and bond markets (low quality bonds) at some point. During that particular week or two we want a portfolio with:

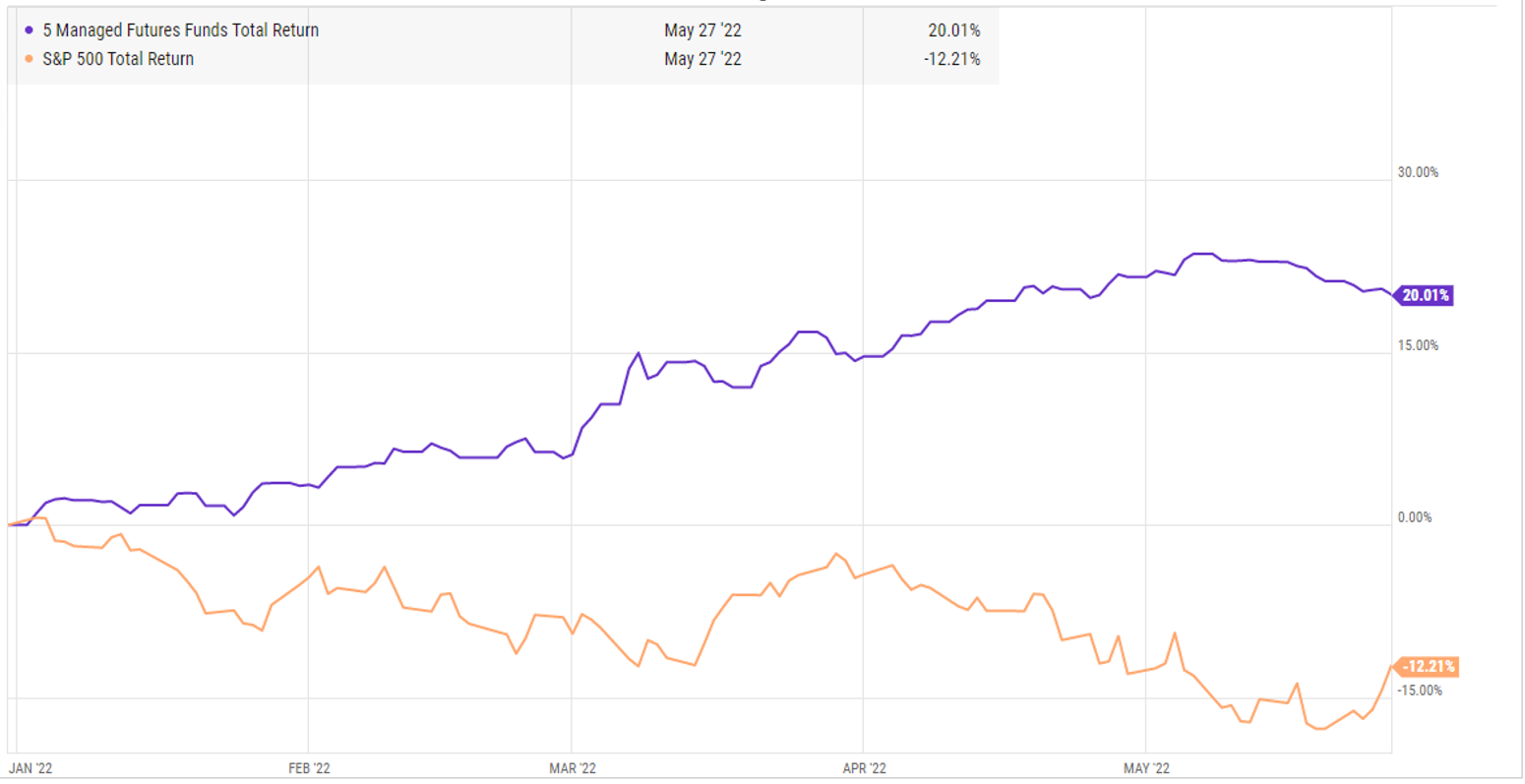

The chart below illustrates the performance of the five managed futures funds we’re presently using at Secure Retirement (equal weighting) versus the S&P 500 stock market index thus far in 2022:

*From YCharts; full report available upon request.

Looking Ahead

Looking Ahead

The same way managed futures funds use probability theory to control their risk and design key parts of their trading programs, I use it both to control portfolio risk and to calculate likely outcomes based on the most trustworthy historical data. Reversion to the mean is the single most important principle which guides most markets over time, and fundamentals suggest that most stocks are still overvalued, and in fact have a long way to fall before they again reach fair value. All this, combined with the burgeoning crises in global markets, leads us to expect the time for “the largest profitable outcomes” for managed futures may be just beginning.